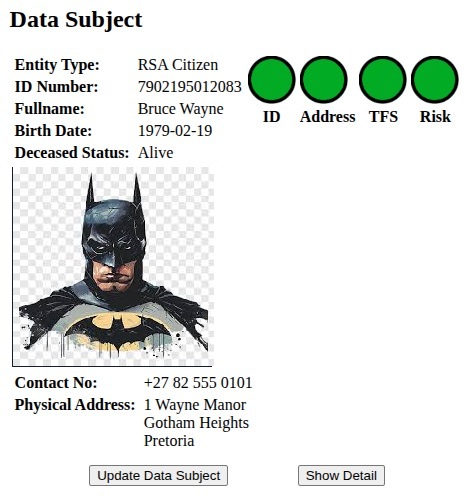

Know-Your-Client (KYC) is a process used by businesses and financial institutions to verify the identity of their clients and assess associated financial crime risks.

KYC, or Know Your Customer/Client, is the start of the due diligence process that organizations use to confirm that clients are who they claim to be. Due Diligence requires that client identities are verified and that clients can demonstrate that they are entitled to the funds they control and to evaluate potential risks associated with these. It is a core component of our risk based approach, covering anti-money laundering (AML) and counter-terrorism financing (CTF) and anti-Proliferation Funding efforts, helping prevent fraud, money laundering, terrorist financing, and other financial crimes. The process ensures that financial institutions and businesses maintain secure and compliant operations while building trust with clients.

Onboarding and Automated BCOS screening

The BCOS system is designed to screen new clients at time of onboarding, and then repeats screening at least every twenty four hours. This rapid and ongoing screening process increases confidence in the accuracy and usability of the data available.

Fast, accurate onboarding allows for enaging with clients confidently.

Onboarding of a new individual takes approximately eight minutes, from initiation up to first Risk Rating. The process is fluid and customizable, which means that impact on workflows are reduced and productivity maintained. This makes BCOS one of the fastest and most sought after products in the compliance and fraud prevention market space.

A key requirement of effective KYC is ongoing monitoring and re-screening. Ongoing monitoring is continuous, which means that when new information becomes available, at any time, the risk profile of a party must be updated. Re-screening requires regular, periodic re-assessment of the risk profile.

Once a profile has been created on BCOS ongoing monitoring and re-screening are background tasks. It is possible, but not necessary for the user to request an update, this is automated by the BCOS system.

Identity Verification

BCOS can provide official government database ID verification. Our unique search and AI enabled risk assessment provides a basic screening within 30 seconds. Yes, it is that fast.

Official Gotham City photo ID.

Identity screening is part of the immediate and initial KYC onboarding.

What exactly is screened?

- Targeted Financial Sanctions (TFS)

- POCDATARA

- National Sanction Lists (NSL)

- Hot Names

- Electronic Footprint (adverse media)

Targeted Financial Sanctions (TFS)

The United Nations Security Council maintains a list of persons and organizations associated with crimes such as weapon smuggling, war crimes and others. These individuals are sanction on a global level and it is illegal to conduct business with the listed parties.

BCOS updates the search criteria within 24-hours of the official UN list being updated, and re-screens all parties listed on the system. This meets ongoing and re-screening requirements. With BCOS it is not necessary to reload an identity onto the system. Once loaded, BCOS does the heavy work.

POCDATARA

Protection of Constitutional Democracy Against Terrorism and Related Acts (POCDATARA) is uniquely South African. BCOS has been screening against a custom POCDATARA list since 2025.

Expected amendments to FICA in 2026 will update the reporting requirements under FICA to treat POCDATARA hits, the same way as TFS hits.

BCOS is ahead of the pack with a full implemented and working POCDATARA screen!

TFS and POCDATARA screening is part of the immediate and initial KYC onboarding.

National Sanctions Lists

South Africa does not maintain a national sanctions list, but most of our major trading partners do. These National Sanctions Lists (NSL) contain the names of persons, organizations, vessels & aircraft that are subject to the sanctions of those states. The implication is that it is illegal in those countries to trade with the sanctioned parties.

For example, the USA Office of Foreign Assets Control publishes a list of individuals and companies owned or controlled by, or acting for or on behalf of, targeted countries. It also lists individuals, groups, and entities, such as terrorists and narcotics traffickers designated under programs that are not country-specific. Collectively, such individuals and companies are called Specially Designated Nationals (SDNs). These appear on several lists, such as Foreign Sanctions Evaders List, the Sectoral Sanctions Identifications List, the List of Foreign Financial Institutions Subject to Correspondent Account or Payable-Through Account Sanctions, the Non-SDN Palestinian Legislative Council List, the Non-SDN Menu-Based Sanctions List, and the Non-SDN Communist Chinese Military Companies List.

South Africa is not directly subject to the jurisdiction of those foreign NSL requirements. However, names are not added to NSL for no reason. It is prudent to extend standard KYC to include these NSL restrictions in order to determine possible increased financial crime risks.

At the moment BCOS screens against the NSL lists published by

- USA

- UK

- EU

- Australia

- Canada

Hot Names

BCOS screens for specific names that are associated with specific roles or functions. Typically the names of Members of Parliament (MP) or Members of Provincial Legislatures (MPL) or other, similar government positions are included. These names are sources from official governments sources and updated as new information becomes available.

Electronic Footprint

Electronic Footprint

An electronic footprint, or digital footprint, or digital shadow, is the sum of traceable digital activities, actions, and communications that users leave online. This includes websites visited, emails sent, social media interactions, online purchases, and any information submitted through digital platforms. This can be both active, such as posts and passive such a media reports. The term adverse media is a subset of the electronic footprint and refers specifically to media reports.

Any online presence can be traced.

Hot Names, NSL and Electronic Footprint screening is part of the second phase of KYC onboarding. The time required from initiation to completing the risk assessment is approximately eight minutes for an individual and the risk assessment process concludes with a risk rating. Life, accurate, online risk assessments available 24/7.

BCOS is typically deployed as part of a complete compliance package, or integrated through our public API into corporate compliance solutions.

If you require more information on BCOS please do not hesitate to contact us.

-Be Compliant

Issued September 2025 and covers 76 pages. This revised document replaces Guidance Note 7A issued in February 2025. This document is essential reading for understanding concepts fundamental to the FICA process. Among other essential topics, it covers Know-Your-Client concepts, Ultimate Beneficial Ownership and developing a Risk Based Approach.

Issued September 2025 and covers 76 pages. This revised document replaces Guidance Note 7A issued in February 2025. This document is essential reading for understanding concepts fundamental to the FICA process. Among other essential topics, it covers Know-Your-Client concepts, Ultimate Beneficial Ownership and developing a Risk Based Approach.